Turn shop-floor credibility into a recruiting engine: build a real EVP, fix candidate experience, enable ambassadors, measure outcomes that matter.

Continue readingTurn shop-floor credibility into a recruiting engine: build a real EVP, fix candidate experience, enable ambassadors, measure outcomes that matter.

Continue reading

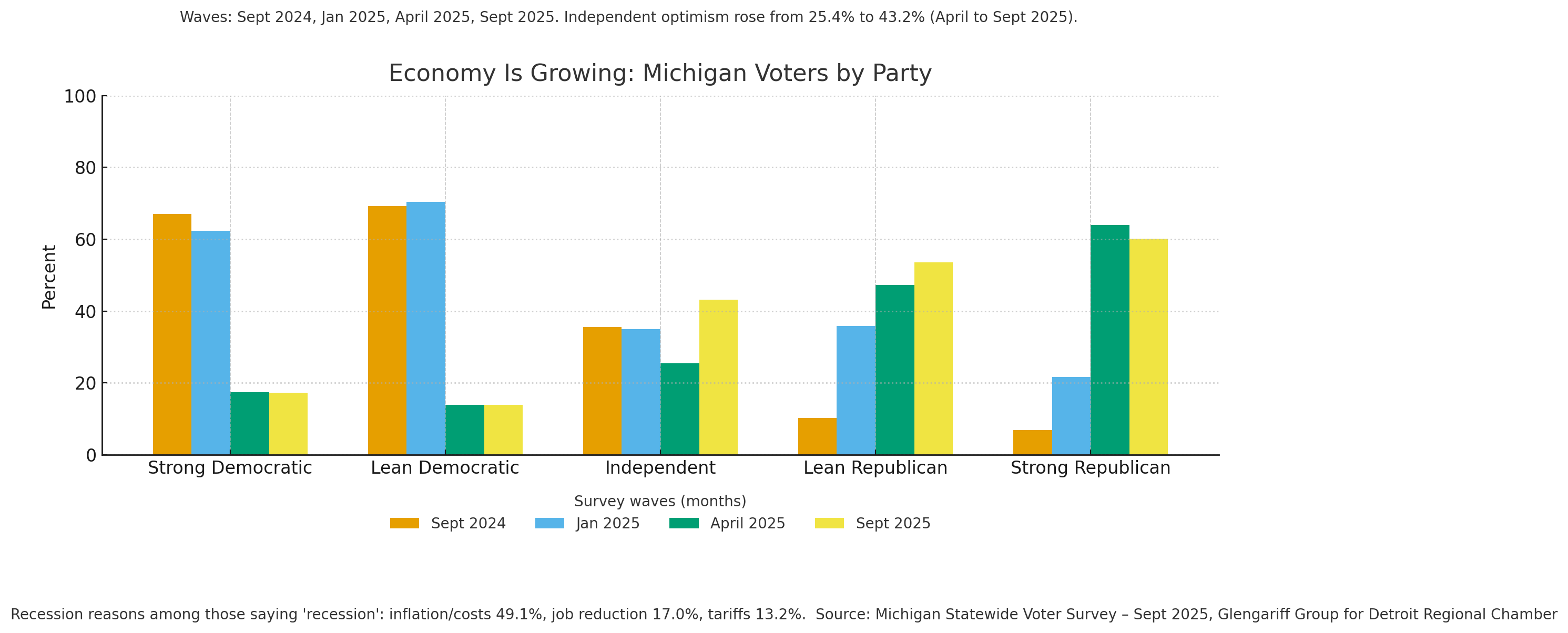

The Detroit Regional Chamber’s September 2025 Michigan Statewide Voter Survey, conducted by the Glengariff Group, offers a snapshot of a state both resilient and restless. The data reveal a public that sees signs of economic stabilization but remains haunted by high costs, uneven opportunity, and deep uncertainty about what lies ahead. Over the next six months, the outlook hinges on whether consumer confidence and job quality can overcome the drag of inflation and tariff pressure.

For the first time since early 2025, more than half of Michigan voters, 51.5 percent, say the state is on the right track, compared to 33.7 percent who believe it is on the wrong one. This modest optimism stems mainly from independents, whose right-track sentiment jumped from 44.7 percent in April to 52.3 percent in September. Strong Republican voters also showed a notable uptick, from 20.9 percent to 34.0 percent. These shifts suggest a fragile coalition of confidence that extends beyond partisan lines, even as economic doubts persist.

But when asked specifically about the economy, Michiganders are divided. Forty-two point four percent say it is on the right track, and 42.8 percent say it is not. This statistical split highlights a state where people may feel better about direction and leadership than about their wallets.

Political identity shapes how people read the same economic facts. This is normal and well documented. Pew shows that views of national economic conditions swing with party control of the White House, with Republicans turning more positive and Democrats more negative in 2025. Gallup reports the same flip in its Economic Confidence Index following the 2024 election, driven by Republicans becoming more upbeat and Democrats more downbeat. Political scientists describe this as motivated reasoning or partisan bias in perception, where people seek and interpret information that affirms prior loyalties rather than updating neutrally.

Inflation remains the state’s defining economic anxiety. Among voters who say Michigan’s economy is on the wrong track, 38.8 percent cite inflation and the cost of goods as the main reason, up sharply from 22.9 percent in May. Three out of four residents, 75.8 percent, report paying more for groceries, two thirds, 68.1 percent, for utilities, and 60.4 percent for home or auto insurance. These figures cut across demographics and party lines.

The pain of rising costs has not translated into universal despair. Roughly 72.6 percent of voters say they are doing better or about the same as a year ago. Yet, of the 27.1 percent who say they are doing worse, a majority, 55.2 percent, blame inflation. Only 16.8 percent say they are doing better, often due to wage increases, promotions, or new jobs, small but meaningful signs of labor-market movement.

Just over half, 52.0 percent, believe good-paying jobs are available, a drop of eight points since May. That decline is led by Democratic voters, only about one third of whom see strong job prospects. Independents, 60.4 percent, and Republicans, roughly two thirds, are more upbeat. Still, four in ten Michiganders say they know someone looking for work, and 77.8 percent of them say it has been hard to find a job. Among those aware of recent college graduates, 77.0 percent say the same.

This sentiment gap, between perceived availability of good jobs and personal experience finding them, underscores a labor market that feels tight on both sides. For employers, it signals lingering competition for skilled workers even as wage pressure softens. For job seekers, especially younger and lower-income workers, it reflects frustration that openings do not always translate into sustainable pay.

Michigan’s manufacturing base feels the bite of global policy more than most. Voters oppose the expanded tariffs by a 51.2 to 40.8 margin. A majority, 71.5 percent, say tariffs have increased what they pay for goods, and 60.3 percent believe tariffs are hurting the state’s auto industry. Nearly half expect smaller profit-sharing checks for auto workers this year.

Those numbers suggest that what was once an abstract policy debate has become a daily reality for Michigan households. The rising costs of vehicles, materials, and inputs are trickling through to local economies. Yet, some blue-collar workers remain more supportive of tariffs than their white-collar counterparts, indicating that the political divide over trade is tied to identity as well as economics.

Nearly half of Michigan voters (47.5%) report using AI in their personal or professional lives, but optimism about its benefits is muted. Only 23.7% believe AI will make Michigan more prosperous, while 39.4% think it will make the state less so. A majority (61.0%) expect AI to lead to fewer jobs, not more Fall-2025-Michigan-Voter-Poll . The divide between white-collar and blue-collar voters is striking: 71.6% of white-collar workers say they use AI, compared to just 36.6% of blue-collar workers. This gap reveals an emerging structural challenge: whether technology adoption will widen or bridge economic divides. If Michigan’s industrial base fails to reskill its workforce at pace with automation, that pessimism could become self-fulfilling.

The Next Six Months: Two Diverging Roads

Optimistic scenario: Inflation continues to cool, tariffs stabilize, and employers—especially in automotive and advanced manufacturing—resume hiring to meet long-term production goals. Wage growth steadies, confidence rises among independents, and consumer spending normalizes into early 2026. Negative scenario: Inflation expectations, already high (43.1% expect it to worsen), drag on real wages. Tariff-driven costs ripple through Michigan’s manufacturing base, curbing output and dampening profit-sharing. Job openings persist, but workers remain mismatched or underpaid. In that climate, optimism could collapse as quickly as it rebounded. The September 2025 survey captures a moment of balance—between endurance and fatigue, adaptation and anxiety. Whether Michigan leans toward renewal or retrenchment will depend less on macroeconomic forces and more on how effectively its employers, educators, and policymakers convert short-term strain into long-term resilience.

Federal shutdown stalls permits, freezes loans, hits tourism and auto supply chains, eroding confidence across Michigan manufacturers, consumers, and businesses.

Continue reading

As the upcoming election draws near, the revitalization of American manufacturing has once again become a central theme in political discourse. Presidential candidates are making ambitious promises to bring back factory jobs and strengthen the industry. However, for manufacturing professionals in Michigan—a state with a rich industrial heritage—the pressing question is: How much can a president truly influence the revival of manufacturing, and what local opportunities are shaping the industry’s future? This recent New York Times article asked that question. In this blog, we examine how the election could affect jobs here in Michigan.

Political Proposals vs. Economic Realities

Former President Donald J. Trump proposes imposing hefty tariffs on nearly all imports to encourage foreign companies to produce goods in the United States. Vice President Kamala Harris, meanwhile, advocates for tax credits and expanded apprenticeships to bolster factory towns and invest in advanced technologies. While these proposals make for compelling campaign narratives, historical evidence suggests that no president can single-handedly dictate the growth of specific industries.

Economic forces such as global market trends, technological advancements, and exchange rates often have a more significant impact on manufacturing. While federal policies can provide incentives and create a favorable environment, the real drivers of manufacturing growth are often found at the state and local levels.

Sun Belt States: The Rise of Business-Friendly Environments

In recent years, manufacturing jobs have been migrating toward the Sun Belt states—such as Texas, Florida, and those in the Southeast—known for their business-friendly climates. These states offer lower taxes, fewer regulations, reliable access to power, and a growing workforce attracted by a lower cost of living and favorable weather.

Nevada, for example, has seen its manufacturing job base grow by more than 13% from early 2020 to March 2023. The state has actively worked to diversify its economy beyond hospitality and entertainment, offering incentives and a welcoming atmosphere for manufacturers. Companies like Alliance North America (ANA) have relocated there, attracted by lower operational costs and a supportive business environment.

“Instead of companies choosing the right location based on all of their other requirements and the presumption that the workers are going to come to them, companies are starting from the presumption of, where are the people moving to?” said Didi Caldwell, president and CEO of Global Location Strategies.

Michigan’s Manufacturing Landscape: Leveraging Local Opportunities

Michigan offers a variety of subsidies and incentives designed to lure businesses and encourage expansion:

Michigan Business Development Program (MBDP): Provides grants, loans, and other economic assistance to businesses that create qualified new jobs and make new investments in Michigan.

Industrial Property Tax Abatement (PA 198): Offers property tax incentives to manufacturers looking to renovate or expand facilities, reducing costs associated with property improvements.

Michigan New Jobs Training Program (MNJTP): Assists employers in training workers for new positions by providing flexible funding to meet the demand for skilled labor.

Michigan Reconnect Program: Aims to help adults over the age of 25 earn a tuition-free associate degree or skilled trade certificate. This program enhances the workforce by providing manufacturers with a pool of skilled workers trained in advanced manufacturing techniques.

Good Jobs for Michigan Program: Provides incentives for businesses that create a significant number of high-paying jobs, aiming to boost the state’s economy and employment rates.

These programs underscore Michigan’s commitment to fostering a business-friendly environment, reducing operational costs, and supporting workforce development—a critical factor for manufacturers considering relocation or expansion.

Case Study: Michigan’s Attractiveness to Manufacturers

Several companies have taken advantage of Michigan’s incentives to grow their operations:

Ford Motor Company’s Electric Vehicle Investment: Ford has announced significant investments in Michigan to expand electric vehicle production, leveraging state incentives to modernize facilities and retrain workers.

LG Energy Solution’s Battery Plant Expansion: In Holland, Michigan, LG Energy Solution is expanding its battery manufacturing plant, supported by state grants and tax incentives aimed at boosting the clean energy sector.

These developments highlight Michigan’s strategic focus on not only preserving its manufacturing legacy but also pivoting towards emerging industries like electric vehicles and renewable energy technologies.

Balancing Local Advantages with National Trends

While the Sun Belt states offer attractive environments for manufacturers, Michigan’s unique combination of incentives, skilled workforce, and infrastructure continues to make it a compelling choice for manufacturing professionals.

Manufacturers in Michigan benefit from:

Skilled Workforce: Michigan boasts a rich pool of skilled labor, thanks to its strong educational institutions and programs like the Michigan Reconnect, which enhances workforce skills by providing tuition-free pathways for adults seeking degrees or certificates in high-demand fields.

Infrastructure and Logistics: The state’s robust transportation network—including major highways, railroads, and ports—facilitates efficient distribution and supply chain operations.

Community and Government Support: Local governments often work closely with businesses to streamline permitting processes and provide assistance, enhancing the ease of doing business.

Cautious Optimism Amid Uncertainty

Despite the positive local factors, the manufacturing industry remains cautious due to broader economic uncertainties and the impending election. Companies are mindful that the outcome could influence taxes, trade policies, and regulations.

“We’re a couple of months away from a huge decision point—who controls Congress and the White House,” said Timothy Fiore, manufacturing business committee chair at the Institute for Supply Management. “I think we’re kind of stuck here until the end of the year.”

Seizing Opportunities in Michigan While Recognizing National Trends

For manufacturing professionals in Michigan, the path to revitalization lies in leveraging state-specific incentives and opportunities while staying aware of national trends like the growth in Sun Belt states. While federal policies and political promises can influence the broader landscape, it’s the tangible, local actions that create a conducive environment for growth.

Michigan’s commitment to supporting manufacturing through various incentives, workforce development programs like Michigan Reconnect, and a business-friendly climate positions it as fertile ground for industry expansion. As the election nears, industry stakeholders should focus on these local advantages, ensuring they are well-positioned to capitalize on the opportunities ahead, regardless of political outcomes.

As we welcome 2024, the landscape of economic forecasts has been in a constant state of flux, especially throughout the holiday season. As we step into the new year, one can’t help but wonder about the prospects of the 2024 US economy. Amidst a stream of headlines, many of which lean towards the positive, we find ourselves sifting through the information – eager to uncover the encouraging trends while also remaining vigilant for any potential challenges that may lie ahead.

Inflation is Under Control

One of the most remarkable aspects of the current economic situation is the successful containment of inflation. For years, concerns about rising prices have dominated discussions, but now we find ourselves in a scenario where inflation is finally under control. In 2023, the annual inflation rate saw a significant decline, falling from its peak of 7.5% earlier in the year to a more manageable 2.6% by November. This marked decrease reflects the effectiveness of the Federal Reserve’s monetary policy and its commitment to price stability.

The core inflation rate, which excludes volatile food and energy prices, also exhibited a noteworthy deceleration. In the same period, core inflation dropped from 5.2% to 3.2%. This demonstrates that the pricing pressures affecting essential goods and services are diminishing, providing relief to American households.

Policymakers at the Federal Reserve have been resolute in their efforts to keep price pressures in check, ensuring that Americans can maintain their purchasing power. Their commitment to a long-term inflation target of 2% has played a pivotal role in fostering stability and predictability in our daily lives. As we look ahead to 2024, the outlook for inflation remains positive, with a well-managed and controlled inflationary environment contributing to the overall strength of the US economy.

The Fed Looks to Hold Longer Than Expected

The Federal Reserve’s decision to maintain higher interest rates for an extended period might initially appear to be a cautious move. Still, it’s important to recognize the wisdom behind it. Since peaking in 2022, the Fed’s favored inflation gauge has fallen sharply, reaching an annual rate of 2.6 percent in November. This marked decrease in the inflation rate is a testament to the central bank’s commitment to its mandate of ensuring price stability.

By resisting immediate rate cuts, the Federal Reserve demonstrates its confidence in the effectiveness of its policies. Rather than reacting hastily to short-term fluctuations, the Fed is taking a deliberate approach to safeguard the economic gains achieved in recent years. This measured stance is essential for maintaining the long-term health and resilience of the US economy, and it provides businesses and consumers with a sense of stability and confidence as we navigate the economic landscape of 2024.

The Job Market Remains Strong

One of the most encouraging aspects of the current economic scenario is the solid job gains. In December, employers added a robust 216,000 jobs, exceeding expectations. Notably, the unemployment rate held steady at a low 3.7%, showcasing a year-over-year improvement compared to the previous year’s 3.5% rate.

Furthermore, manufacturing jobs, a critical component of the U.S. economy, have continued to play a pivotal role. While the overall job market is thriving, manufacturing employment has shown resilience, with the average workweek remaining largely unchanged at 39.8 hours in December. Overtime in manufacturing also remained consistent at 2.9 hours. Although manufacturing employment experienced some fluctuations in 2023, it remained a crucial contributor to the nation’s workforce, supporting the broader economic growth story.

As we embark on a new year, it’s clear that the United States is in an enviable economic position. Inflation is under control, the stock market is factoring in measured rate cuts, and job gains remain solid while unemployment stays low. When we ask, “What’s the Bad News?” it’s challenging to find significant negative aspects in our current economic landscape. This positivity is a testament to the resilience, adaptability, and strength of the US economy. As we move forward, we can appreciate the strides we’ve made and face any potential challenges with confidence and determination.

So What’s the Bad News?

Even though the traditional measurements for economic health remain relatively strong, there are underlying issues that linger beneath the economic shine:

The US debt pile surpassed $33 trillion in 2023, up more than $3 trillion during the year and $10 trillion since 2019, the last calendar year before the COVID-19 pandemic. Meanwhile, the latest Congressional Budget Office (CBO) projections point to a budget deficit that will be above 5% of gross domestic product (GDP) for the next ten years.

At this rate, the amount of US government debt could surpass $50 trillion by 2033. This, at a time of higher interest rates (at least for now), could mean that, by 2031, the country spends more on interest payments than it does on non-defense discretionary expenditures (such as funding for transport, education, health, international affairs, natural resources and the environment, and science and technology). This is unsustainable.

Manufacturing also seems to be struggling to grow in these uncertain times, but remains resilient. There is also a gap in perception between the reduction of inflation and what people are actually feeling at the cash register.

Even though the numbers are trending in the right direction and gas (at this moment) is under $3 per gallon, there is a discrepancy between the actual economic conditions and public perception, particularly regarding inflation. Many Americans feel that the economy and inflation are worse than they actually are.

And finally, The US economy’s projected performance in 2024 suggests modest growth, with an expected real GDP increase of only 1.0%, a deceleration from the 2.4% growth anticipated in 2023. This forecast, as reported by Barclays Investment Bank and Barclays Private Bank in November 2023, indicates a slowing economy compared to previous years. In 2022, the GDP growth was 1.9%, with consumer price index (CPI) inflation at 8.0%, and the unemployment rate at 3.6%. Looking ahead to 2024, the CPI inflation is forecasted to ease to 2.6%, while the unemployment rate is expected to slightly increase to 4.2%. The gross public debt is projected to rise to 126.2% of GDP, up from 122.0% in 2022 and 123.2% in 2023. Private consumption, which was at 2.5% in 2022, is anticipated to further slow down to 1.1% in 2024. Despite these modest figures, the US economy’s performance still compares favorably with many European nations.

As we approach the new year, there is a blend of encouraging news and the usual uncertainties. Let’s maintain a steady course, fostering a spirit of optimism and hope, as we continue to propel forward on this journey.

Ford’s $3.5 billion EV battery plant in Marshall faces uncertainty amid the UAW strike. Despite the recently announced pause, Michigan’s manufacturing industry remains resilient, boasting a skilled workforce, innovation, and a commitment to securing its place in the electric vehicle revolution. Confidence in the state’s future endures.

Continue reading

Opinions and biases are changing towards those with felony convictions re-entering the workforce. According to a study from the Charles Koch Institute, over 80% of managers and two-thirds of HR professionals felt that workers with criminal records bring just as much (or greater) value to an organization as workers without records.

Continue reading

"*" indicates required fields